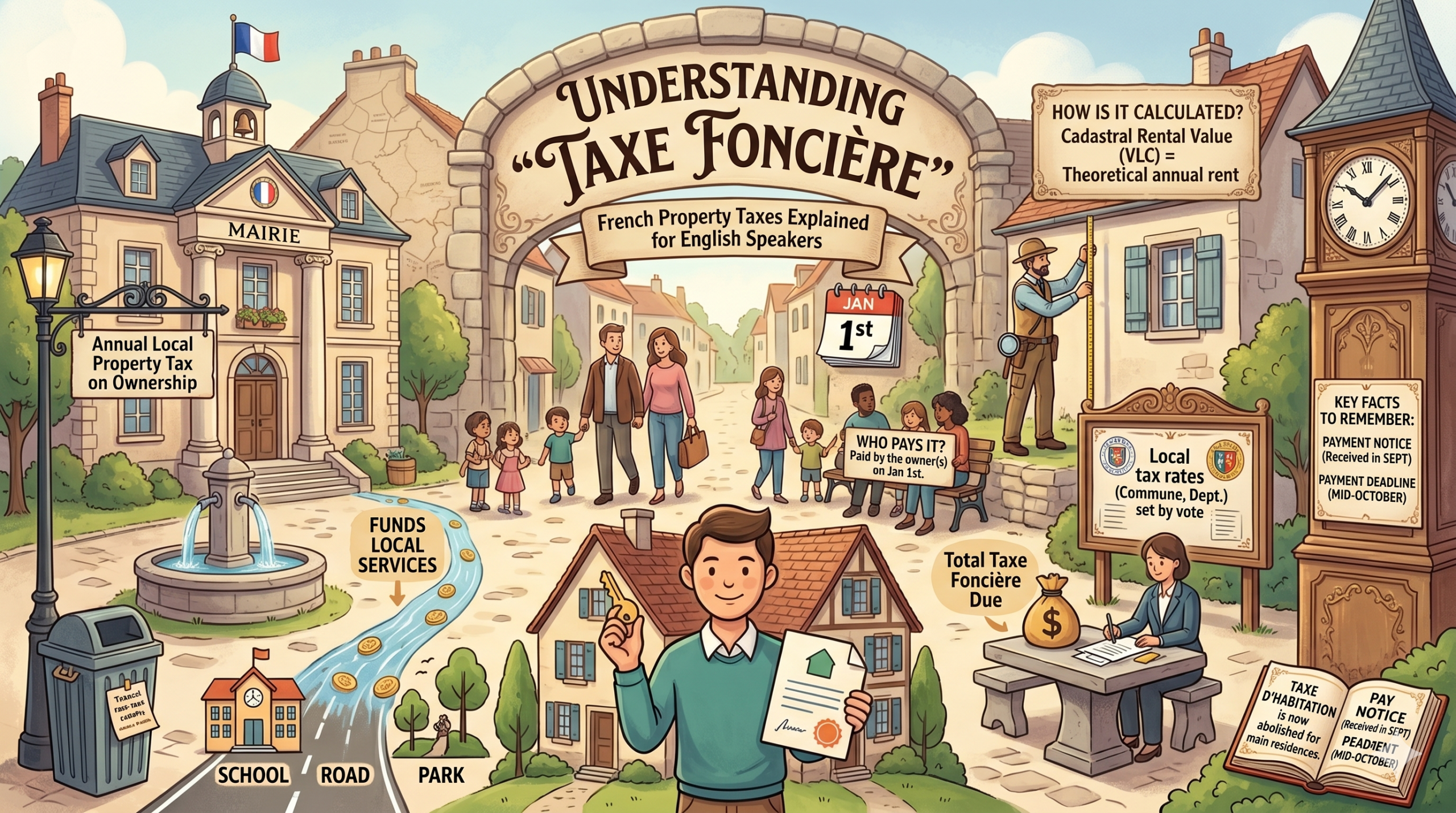

French Property Taxes for English Speakers: Taxe Foncière Explained (2026)

Most anglophone owners discover French property taxes the hard way: a notice arrives in late August, in administrative French, and the rules already moved while they were skim-reading. Here is how the taxe foncière actually works in 2026, what you will pay, and how it compares with the US, UK, and Canada.

The trap nobody flags about French property taxes

Most anglophone owners who get burned by the French property tax system don't get burned because the rates are high. They get burned because the bill follows ownership on 1 January, full stop, no proration. If you sell on 14 March, you still owe the entire 2026 taxe foncière. Buyer and seller usually split it privately in the deed, but the tax office only chases the registered owner. That detail breaks the mental model an American or British buyer arrives with.

🇺🇸 I am the owner on January 1st, 2026.

That sentence, on the deed and in the tax office's database, is the only legal trigger. Not your address. Not how many months you lived there. Not whether the property was rented, empty, or being gutted. The official source for everything that follows is impots.gouv.fr, available in English under the International tab. Bookmark it now, before the August notice arrives.

If the broader administrative landscape is still hazy, our guide to moving to France from the USA walks through visa, registration, and tax-residence basics in order. Property tax is one piece of a larger machinery, and it pays to see the machine.

Taxe foncière vs taxe d'habitation: stop confusing the two

France used to have two property-related taxes hitting nearly every home. Since 2023, the taxe d'habitation has been abolished on primary residences. It still exists on second homes (résidences secondaires), where about 3.7 million owners receive a bill each November, with an average around 1,125 €.

So in 2026, an English-speaking owner sits in one of three boxes: paying only taxe foncière (primary residence in France), paying both taxes (second home), or paying both plus a hefty surcharge (second home in a so-called zone tendue). Around 5,000 communes can now add a surtaxe of 5% to 60% on the taxe d'habitation for second homes. Coastal towns, ski resorts, Paris, and most of Brittany apply the maximum 60%.

🇺🇸 You are liable for the second-home occupancy tax.

🇺🇸 Your commune applies a 60% surcharge.

🇺🇸 Primary residence, second home, or vacant property?

How taxe foncière is actually calculated in 2026

The formula looks deceptively simple:

Taxe foncière = (Valeur locative cadastrale × 50%) × Taux global

Three pieces matter. The valeur locative cadastrale (VLC) is a theoretical annual rent that the tax office estimates your property could fetch. Most VLCs were set in the 1970s and have only been indexed since, which is why they often look bizarrely low compared with real market rents. A 50% standard abatement is then applied to cover assumed maintenance. The result is multiplied by the taux global, voted yearly by the commune, the intercommunalité, and (sometimes) the département.

🇺🇸 Cadastral rental value revalued for 2026.

🇺🇸 Indexation coefficient: +0.8% in 2026.

🇺🇸 Taxable base after the 50% abatement.

For 2026, the VLC is uplifted automatically by +0.8%, indexed on inflation (down from +3.9% in 2024 and +7.1% in 2023). The full general revaluation has been pushed to 2031; a separate update of éléments de confort across 7.4 million homes was suspended on 26 November 2025. If you bought thinking the cadastral system was about to be modernised, plan for the old logic to hold for years.

The structural anomaly

France charges expensive homes surprisingly little because the VLC has not tracked the housing market in five decades. A renovated Marais apartment worth 1.5 million € can carry a smaller taxe foncière than a 300,000 € house in a small town with an aggressive taux global. This is one reason why a Paris flat looks tax-friendly on paper compared with a New Jersey suburb.

The taux global is where bills diverge wildly. Most towns sit between 25% and 45%. Paris voted a 52% rate hike in 2023 and now applies 13.8%, still unusually low for political reasons. Identical apartments in Paris and a small town nearby can produce taxe foncière bills differing by a factor of three. If the term commune itself is unfamiliar, our guide to the Fifth Republic's political layers explains why so many local bodies share the tax pie.

How much you will actually pay

The order of magnitude matters more than the formula. Here is a worked example for a typical owner-occupied home in 2026:

Worked example

A 70 m² Paris apartment with a VLC of 7,700 €/year. Taxable base = 7,700 × 50% = 3,850 €. Paris taux global = 13.8%. Annual taxe foncière ≈ 531 €. The same apartment in a commune with a 35% taux global would pay around 1,348 €. Same building, same square meters, same income for the State, very different bill.

Across France, the average taxe foncière sits between 800 € and 1,200 € per year for an apartment, and 1,200 € to 2,500 € for a house, with strong regional variation. The Union Nationale des Propriétaires Immobiliers tracks an average increase of +37.3% over the past decade. Building the French to read your own notice without translation tools is the single highest-leverage skill here, and that is exactly what a structured habit like the French Progress Pass targets: institutional French, daily, without the scattered apps. From there the rest of the bureaucracy stops being a foreign language.

🇺🇸 Amount due before October 20, 2026.

🇺🇸 You are on the monthly direct-debit plan.

🇺🇸 Notice received in your personal account.

🇺🇸 Balance remaining after monthly direct debits.

Calendar, démarches, and the official links you need

French property tax follows a strict autumn rhythm. For 2026, the schedule mirrors 2025, with dates confirmed by the DGFiP each summer. Missing the online deadline by a day triggers a 10% penalty automatically.

-

1Late August 2026 Taxe foncière notice (avis) appears in your impots.gouv.fr account. Mid-September if you are on monthly direct debit.

-

215 October 2026 Payment deadline by cheque, bank transfer, or cash at a partner counter.

-

320 October 2026 Online payment deadline (impots.gouv.fr or the mobile app).

-

4Early November 2026 Taxe d'habitation notice for second-home owners.

-

515 December 2026 Taxe d'habitation deadline (cheque, transfer).

-

620 December 2026 Online deadline for taxe d'habitation.

🇺🇸 The notice arrives in late August, payment is due in mid-October.

🇺🇸 Sign up for direct debit at maturity to avoid the 10% penalty.

🇺🇸 Notice available in your personal account.

Setting up a French bank account is non-negotiable for SEPA direct debit, the smoothest way to pay. The three official links to bookmark are in the Sources at the end of this guide.

Exemptions, reductions, and how to challenge a bill

The system has built-in reliefs that English speakers rarely know about. New constructions are exempt for the first two years after completion (article 1383 of the General Tax Code). Owners over 75 with a revenu fiscal de référence below 11,885 € for one tax-share are fully exempt; between 65 and 75 with the same income limit, a 100 € automatic reduction applies. Energy-efficient renovations and BBC-labelled buildings can win 50% to 100% local exemptions.

🇺🇸 Two-year temporary exemption for new construction.

🇺🇸 Tax relief for elderly residents.

🇺🇸 Reference taxable income below the threshold.

« La taxe foncière fait partie des impôts les plus importants pour les collectivités locales. »

French property tax vs USA, UK, and Canada

The question most English-speaking owners ask is "is France more or less expensive?" The honest answer: France is middle of the pack, but the structure differs sharply from what you know.

| Country | Average annual amount (2026) | Effective rate | Paid by | Reassessment |

|---|---|---|---|---|

| 🇫🇷 France | 800–2,500 € depending on type and commune | ~0.3% of market value (highly variable) | Owner only | Cadastral, frozen since 1970s; revaluation pushed to 2031 |

| 🇺🇸 USA | $2,040 (SC) to $8,920 (NJ) on a $400k home | 1.01% national average; 0.28% (HI) to 2.14% (NJ) | Owner (often via mortgage escrow) | Frequent, state-dependent |

| 🇬🇧 UK | £2,392 Band D England 2026-27 | Flat banded system based on 1991 values | Occupier (owner or tenant) | 1991 (England) / 2003 (Wales) |

| 🇨🇦 Canada | ~$2,800 (Vancouver) to ~$8,000 (Winnipeg) on $1m home | 0.28% (Vancouver) to 2%+ (some Atlantic cities) | Owner | Every 4 years (Ontario, MPAC) |

Two things stand out. First, France has the lowest effective rate in this group, but that is an artifact of frozen VLCs, not a deliberate tax-friendly policy. Second, France is the only one where the tax follows the owner, not the occupier. UK landlords renting their property are rarely on the hook for Council Tax; French landlords are always on the hook for taxe foncière.

The compounding effect

American owners often face higher headline rates but enjoy regular reassessments that smooth out the relationship between bill and market. French owners enjoy lower headline bills but live under a 50-year-old cadastral grid that distorts who pays what. Neither system is fairer in the abstract; they fail and succeed in different places.

If you are a non-resident owner

Non-residents pay the same taxe foncière as residents, but several extra rules apply. Rental income is taxed in France at a 20% minimum, plus social charges that rose to 18.6% on 1 January 2026 (up from 17.2% under the LFSS 2026). EEA, Swiss, and UK nationals affiliated to home social security pay only the 7.5% solidarity levy. The Impôt sur la Fortune Immobilière (IFI) wealth tax kicks in on net French real estate above 1.3 million €.

🇺🇸 You are a non-resident for French tax purposes.

🇺🇸 Social charges applicable to property income.

🇺🇸 Capital gain on the sale of the property.

🇺🇸 Accredited tax representative is mandatory.

🇺🇸 Real estate wealth tax on net assets.

Capital gains on a sale are taxed at 19% plus social charges, with a new accelerated taper from the Loi de Finances pour 2026: full income tax exemption now after 17 years (down from 22), social charges still tapered out over 30 years. The US-France tax treaty and Foreign Tax Credit usually prevent double taxation for Americans, but you must still file in France. Above 150,000 € sale price and outside the EEA, an accredited représentant fiscal is mandatory.

Where Americans get caught

The Foreign Tax Credit prevents double taxation on income, but it does not apply to French wealth tax (IFI). A US owner with two French properties worth 1.5 million € net pays IFI on the slice above 1.3 million €, with no offset on the US side. Plan for it.

Verify everything against the official non-residents portal on impots.gouv.fr, not blog summaries. Treaty interpretations and rates change with each Loi de Finances.

The French you need to read your tax notice

A glossary of the terms that appear on every official document. Memorising these turns the August notice into a 10-minute task.

| French term | English translation | Usage context |

|---|---|---|

| Avis d'imposition | Tax notice | Document received late August, payment due mid-October |

| Valeur locative cadastrale (VLC) | Cadastral rental value | Theoretical rent set by tax office, foundation of every calculation |

| Base d'imposition | Taxable base | VLC × 50% abatement, before applying the taux global |

| Taux global | Combined tax rate | Voted yearly by commune + intercommunalité, varies wildly |

| Date limite de paiement | Payment deadline | 15 October by cheque, 20 October online |

| Mensualisation | Monthly direct debit | Spreads the bill over 10 monthly payments, opt-in |

| Prélèvement à l'échéance | Direct debit at due date | Single auto-payment on the deadline, avoids the 10% penalty |

| Dégrèvement | Tax relief or reduction | Applies to seniors, low income, energy-efficient renovations |

| Réclamation | Formal challenge or appeal | Filed before 31 December of the year following the bill |

| Résidence principale | Primary residence | Taxe d'habitation abolished since 2023 on this category |

| Résidence secondaire | Second home | Still taxed via taxe d'habitation, potential 60% surcharge |

| Logement vacant | Vacant property | Triggers a separate tax in zones tendues |

| Zone tendue | Housing-pressure zone | Coastal towns, ski resorts, Paris: allow second-home surcharges |

| Revenu fiscal de référence (RFR) | Reference taxable income | Threshold used to qualify for relief, capped per tax-share |

| Espace particulier | Personal taxpayer account | Where notices, payment, and biens immobiliers declaration happen |

| Représentant fiscal | Accredited tax representative | Mandatory for non-EEA owners selling above 150,000 € |

Reading your first taxe foncière notice in French is one of those moments when admin vocabulary stops being abstract. If you want to build that habit beyond tax season, our Learning Center has the full ladder of expat-facing topics, and the political vocabulary guide is the natural next step for understanding why your commune voted a particular taux.

Quick answers: French property tax FAQ

Do foreigners pay property tax in France?

Yes. Anyone who owns property in France pays the taxe foncière, resident or not. Non-residents also face a minimum 20% tax on French rental income plus social charges (7.5% if you are affiliated to social security in the EEA, UK or Switzerland, otherwise 18.6% since January 2026), and the IFI wealth tax on French real estate worth more than 1.3 million euros.

Is the taxe d'habitation still a thing?

It was abolished on primary residences in 2023. It still applies to second homes, where owners get a bill each November (around 1,125 euros on average), and roughly 5,000 high-demand communes add a surcharge of 5% to 60% on top.

Who pays the taxe foncière, the owner or the tenant?

The owner, based on who holds the property on 1 January of the tax year. A tenant never pays taxe foncière. Renters used to pay the taxe d'habitation, but that is gone on main homes.

How much is the taxe foncière per year?

Roughly 800 to 1,200 euros for an apartment and 1,200 to 2,500 euros for a house, with heavy regional variation. It is based on the property's cadastral rental value, halved, then multiplied by the local rate. The national average has climbed about 37% over the past decade.

When does the bill arrive and when is it due?

The taxe foncière notice lands in the autumn, with payment usually due in mid-October (a little later if you pay online). Always check the exact deadline printed on your avis.

Can you lower or contest your taxe foncière?

Sometimes. New builds can be exempt for the first two years, low-income owners over 75 may qualify for relief, and you can challenge an incorrect valuation through your local tax office before the deadline on the notice.

Go further

Stop making the same 21 French mistakes. Play them away.

300 pages of games, riddles and quizzes built around the 21 mistakes English speakers actually make in French. You fix them by playing, not by memorising rules. By Camille Aubert.

📚 Keep building in the Learning Center

Imparfait vs Passé Composé Explained: Timeline Method

Imparfait vs passé composé trips up every English speaker because English never forces the same choice. You say…

Read →French Subjunctive Made Simple for English Speakers

The French subjunctive has one job: it marks that something is filtered through a mind, not stated as…

Read →How to translate French politeness (tu vs vous) into English contexts — complete guide

Master the challenge of translating French tu/vous distinctions into English, learn how English expresses politeness without formal pronouns,…

Read →